Consider a scenario: you've prepared. You have food, water, generator fuel, cash, and a solid plan.

Your supplies are in the basement. The basement is flooded.

Or: your supplies are in the garage. The garage door is electric and the power is out. The manual release handle broke six months ago and you never replaced it.

Or: your supplies are at your secondary property three hours away. The highways are closed.

The reserve isn't the plan. Access to the reserve is the plan. These are different things, and most preparation addresses only the first one.

The access problem has three layers:

Physical access. Where are the supplies? Can you reach them without power, without a vehicle, without normal infrastructure? A basement is excellent for storage in every scenario except flooding — which is precisely when you most need what's stored there. Ground level or above, in a structure that stays accessible when the most likely failure modes occur.

Operational access. Can you use what you have without your normal tools? An electric can opener is useless without power. A gas stove requires a pilot light or manual ignition. A propane stove requires knowing where the connection is and how to light it. Run through the operational chain once, without the tools you'd normally rely on, before you need to do it under stress.

Informational access. Do other household members know where things are and how to use them? The prepared person is not always the person who will need to access the supplies. Your partner, your teenager, a trusted neighbor — if they don't know the location, the combination, and the operating procedures, the preparation is a single point of failure wearing the costume of redundancy.

The mobility problem.

Ukraine 2022 is the clearest case: the families who evacuated successfully weren't the ones with the most supplies. They were the ones who could move with what mattered and leave the rest.

Mobility requires a different kind of preparation than stationary resilience. The 72-hour bag — genuinely packed, genuinely portable, genuinely accessible at 3 AM — is a different asset class than the fully stocked basement. You need both. They serve different scenarios.

The stationary reserve handles: grid failure, supply chain disruption, short-to-medium duration events where you shelter in place. The mobile kit handles: evacuation, displacement, scenarios where you need to leave and the supply chain at the destination is uncertain.

Most people prepare for one and assume the other will sort itself out. It usually doesn't.

The last-mile financial version.

Your net worth is substantial. It's in equity accounts, real estate, retirement funds, and a checking account. In a genuine crisis, the assets that help you are the ones you can access and deploy in 24–72 hours.

Equity accounts: typically T+1 settlement since May 2024, then a wire transfer that takes a day. Not accessible in 24 hours.

Real estate: weeks to months to transact. Illiquid by definition.

Retirement accounts: accessible with penalty, taxable event, and a processing time that assumes a functioning financial system.

Cash on hand: immediate. No settlement. No transfer. No counterparty.

The last-mile financial problem is the gap between what you have on paper and what you can deploy when the infrastructure is constrained. Most high-net-worth households are extraordinarily well-positioned for normal market conditions and meaningfully illiquid in a 72-hour crisis.

Sizing the liquid position — the kind that works when the card reader doesn't — is the last-mile trade. Small relative to the portfolio. Disproportionately important when it matters.

The unit door matters less than whether you have the key, can reach the unit, and have already told your family where it is.

That's the last mile. Most people skip it. Most people also assume they won't need it.

Both things can be true until they aren't.

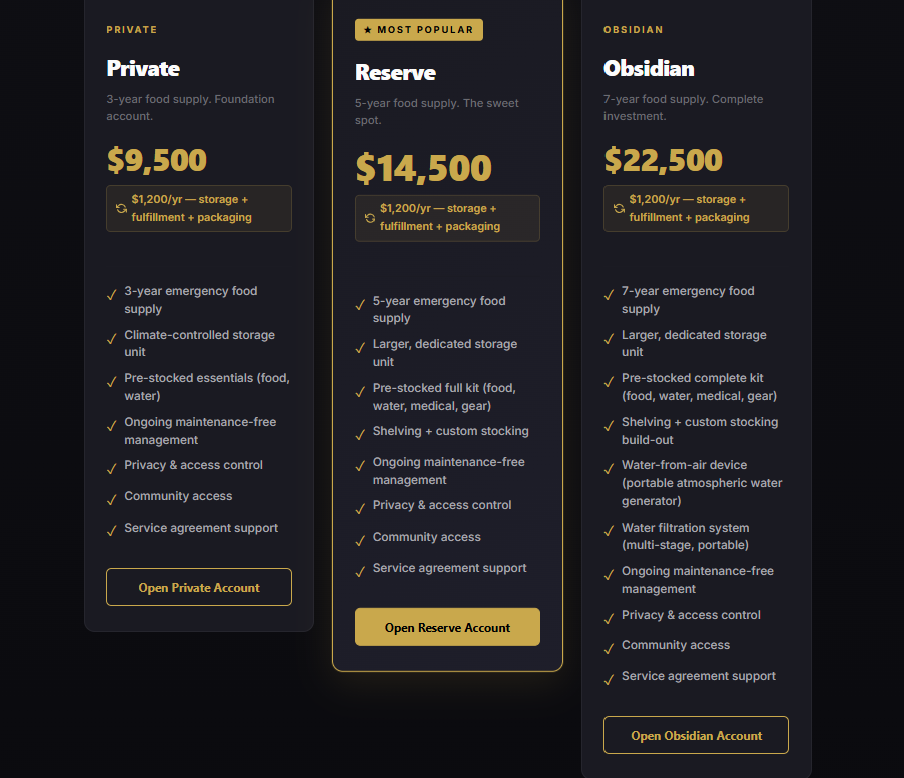

StokdUp positions reserves where they can be reached — managed, maintained, and accessible when the scenario actually arrives. Membership is by reservation.